Splitting bills 50/50 would seem fair, but it may be the most unfair method of doing so. My analysis shows that you may be adding financial stress and hurting your own ability to save when using the 50/50 method.

The 50/50 Method

The most common method for splitting bills is just to split everything 50/50. Simply take each recurring bill and divide the amount by two. $1,500 for rent equals $750 each. $200 for electric equals $100 each. And so on for every recurring bill.

There is Always That One Roommate or Boyfriend

With the 50/50 method, you would think roommates or couples would never argue about splitting bills this way! However, there is always the roommate that takes a 15-minute shower, cranks the heat or the AC, or the boyfriend that always leaves the lights on when he goes out. I am not even going into food and alcohol consumption issues!

Roommates vs. Spouses/Partners

Roommates have no vested interest in the other’s finances beyond splitting the bills. If the roommate is not saving for retirement, carrying credit card debt, or has large student loan payments, that’s their problem. Conversely, married and cohabitating couples do have a vested interest in the other’s finances. Saving for retirement, reducing debt, and building a life together should be common goals. Thus, these couples need to take a holistic approach to their finances.

The Risk of the 50/50 Method for Spouses/Partners

While the 50/50 method makes sense for roommates, it can be risky for couples.

Let’s look at an example where your take-home pay is $4,000 a month and your significant other’s take-home pay is $6,000 a month. Next, let’s assume you’re splitting $5,000 in monthly bills. Following the 50/50 rule, you are each contributing $2,500 towards your monthly bills.

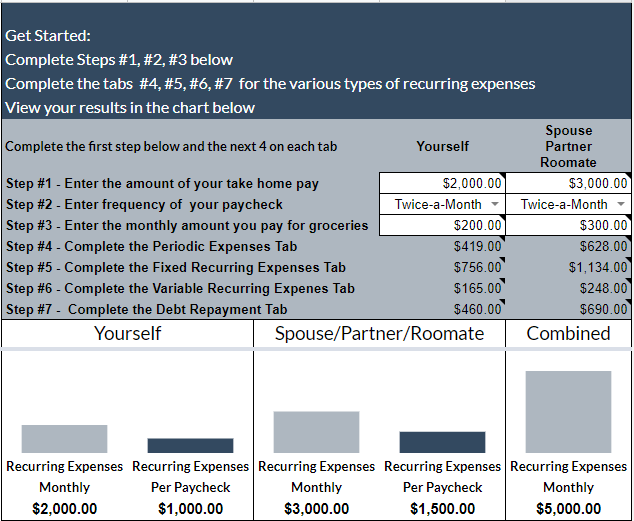

Click the image or link above to get your free copy of my spreadsheet.

However, as a percentage of take-home pay, you are contributing 63% of your monthly take-home pay towards the monthly bills. Conversely, your significant other is paying only 42% of their take-home pay towards the monthly bills. This could lead you to have little money left over for discretionary expenses and savings. Also, your significant other may not understand any money issues your family faces, as they have plenty of money left over each payday for discretionary expenses and savings.

Click the image or link above to get your free copy of my spreadsheet.

The Random Bill Method

In this method, you pay 100% of some recurring bills and your significant other pays 100% of other recurring bills. This method is usually used by couples who have not opened a joint account together. Your risk under this method is typically the same as the 50/50 method. You may wind up paying more than 50% of your take-home pay for the bills you are paying, leaving you little money for discretionary expenses and savings.

The Percentage of Take-Home Pay Method

A better method for splitting your monthly bills is to use the percentage of take-home pay. Based on the example above, you would contribute 40% ($4,000/$10,000) and your significant other 60% ($6,000/$10,000) of take-home pay towards the monthly bills.

Click the image or link above to get your free copy of my spreadsheet.

Using this method, you will now pay $2,000 ($5,000 x 40%) and your significant other will pay $3,000 ($5,000x 60%) a month towards the family’s needs. This gives you an extra $500 a month to allocate towards discretionary expenses and savings. Conversely, since your significant other has $500 a month less to spend, they may be more aware of their spending on discretionary expenses.

Click the image or link above to get your free copy of my spreadsheet.

100%/100% Method That My Wife and I Personally Use

When my wife and I were engaged, we discussed our desire for her to be a stay-at-home mom to raise our children. From day one of our marriage, we started preparing to be in a financial situation to make this happen. We used 100% of my paycheck to pay all of our bills and we saved 100% of my wife’s paycheck. We did this for the first 3 years of our marriage. Per our plan, my wife stopped working when our daughter was born. Shortly afterward, we purchased our home with a 40% down payment from saving my wife’s paychecks.

Fast forward 15 years and with our kids in school, my wife returned to teaching on a part-time basis. Once again we went with the 100%/100% method. We continued to live on my paycheck and save her entire paycheck. As our second child was getting ready to graduate from college, we were able to purchase our vacation home with a $100,000 down payment from the saving of my wife’s paychecks.

A Joint Bank Account for Spouses/Partners

Back in the day when I got married, couples typically closed their individual accounts and merged all of their money into joint bank accounts. Today this is less likely. While I can see keeping some accounts separate, you should have at least one joint bank account for the paying of your recurring bills. If you haven’t already opened at least one joint bank account, now is the time to do it. See my previous post on this topic via the link below.

Conclusion

While splitting your bills 50/50 seems to be the most logical method for couples, you may actually be penalizing one spouse vs. the other. Take a look at the percentage of take-home pay method and see how this method would change things for you. Having open and honest conversations about sharing your bills can reduce your stress levels, help you establish joint saving goals, and improve your overall financial well-being.

Readers, how do you share the cost of your recurring expenses? How did you decide on this approach? Do you have any examples or stories you can share? If so, please leave a comment below.

Leave a Reply